The prospect of a £549 weekly State Pension has captured the attention of millions across the United Kingdom. For retirees and those approaching their sixties, this figure represents more than just numbers—it reflects financial security, dignity, and the ability to live comfortably amidst rising living costs. While the current State Pension system provides a foundation, many argue that it falls short of covering the true cost of modern retirement.

The Current UK Pension Landscape

To understand the significance of a £549 weekly payment, it is important to examine the present framework. The UK’s State Pension is divided into two categories: the Basic State Pension and the New State Pension, which applies to those who reached pension age after April 2016. Even at its maximum rate, the New State Pension remains well below £500 per week.

The government’s Triple Lock mechanism ensures that pensions rise annually in line with inflation, average earnings, or a minimum of 2.5%. While this provides some protection against rising costs, the gap between the statutory minimum and a genuinely comfortable retirement remains substantial. Many pensioners find their weekly payout covers essentials but leaves little room for unexpected expenses or discretionary spending.

The Origin of the £549 Figure

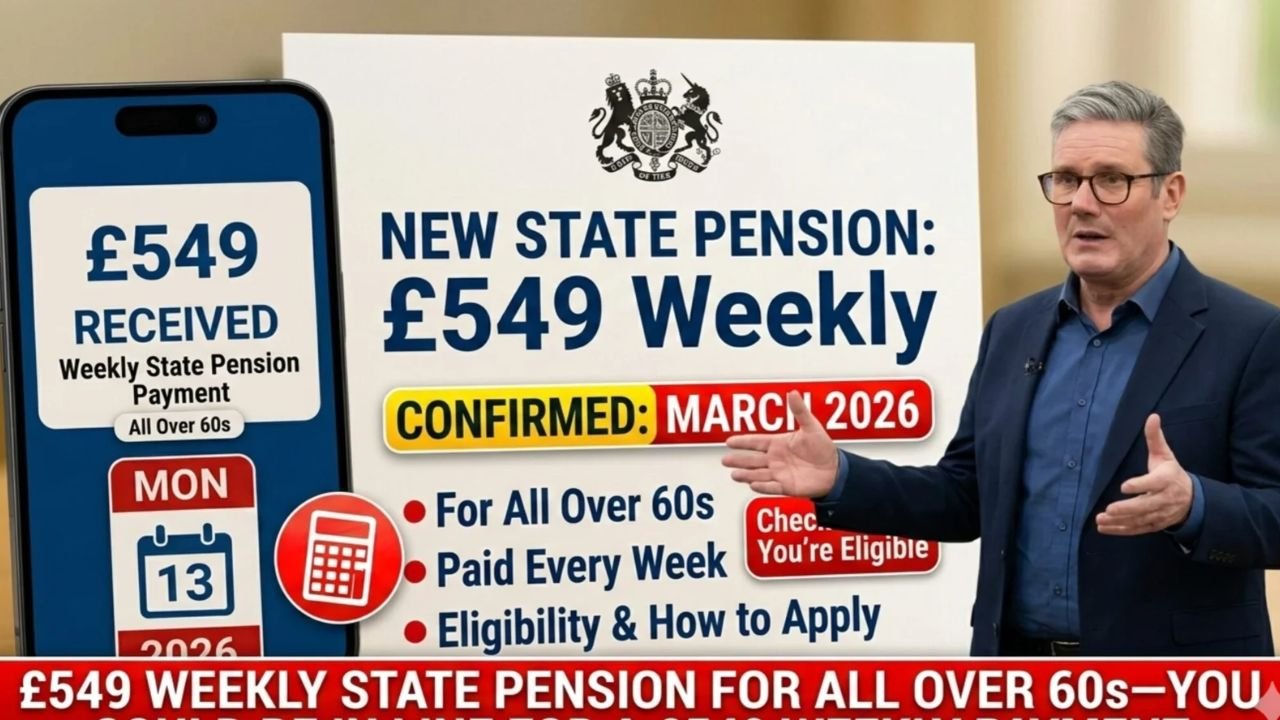

The £549 figure has emerged largely through advocacy campaigns and social discussions highlighting the UK’s relatively modest pension compared to other developed nations. Proponents argue that to align the State Pension with average earnings or a “living wage” standard, weekly payments would need to reach around £500–£550.

This number is framed as a “Living Pension”, designed to ensure that no person over 60 struggles with fuel poverty or cannot afford nutritious food. It represents a vision of retirement that prioritizes financial independence and dignity.

Debating the Pension Age

A core element of this proposal is the lowering of the pension age to 60. Currently, the State Pension age is gradually rising toward 67 and eventually 68. Advocates for a £549 weekly payment argue that early retirees, particularly those who have performed physically demanding work or face health challenges, deserve a secure income without the pressure of remaining in the workforce.

Critics, however, highlight that many over-60s are still active contributors to the economy. Balancing early access with sustainability and workforce participation is central to the debate.

Addressing the Cost of Living Crisis

The UK has faced significant cost-of-living pressures in recent years, with energy, food, and housing costs rising disproportionately for fixed-income households. A £549 weekly pension would dramatically increase disposable income for many pensioners, allowing them to cover essentials comfortably.

Beyond individual benefits, this income boost could stimulate local economies. Pensioners typically spend locally, supporting shops, services, and community businesses. Economists often view higher pensions as a form of direct economic stimulus.

Challenges to Implementation

Implementing a £549 weekly pension presents major financial and policy challenges. The State Pension is already one of the largest expenditures on the government’s balance sheet. Funding a substantial increase would likely require:

- Tax reforms, including higher National Insurance contributions.

- Adjustments to Income Tax rates for higher earners.

- Potential restructuring of the pension funding system.

Intergenerational fairness is also a concern. Younger workers, managing housing costs and student debt, may resist bearing the tax burden for significantly higher payouts to older generations.

International Comparisons

When compared globally, the UK pension system often appears modest. Countries like France, Spain, and the Netherlands provide structures linked to previous earnings, resulting in higher quality of life for the elderly. Advocates for a £549 weekly pension frequently reference these comparisons, emphasizing that other nations successfully support retirees at higher levels without collapsing their economies.

The Triple Lock and Future Raises

The Triple Lock mechanism remains the main driver of pension increases. While it does not produce a £549 weekly payment instantly, it prevents pensioners from falling further behind. Political debates continue over whether to maintain, modify, or replace the Triple Lock, with potential reforms influencing any future increase.

For those over 60, the survival of the Triple Lock is critical. Any movement toward a higher weekly payment would likely involve adjusting this formula, potentially linking pension growth more directly to national wage increases.

Supplementing Income Today

While a £549 pension is not guaranteed, there are existing benefits that can help bridge the gap:

- Pension Credit: Provides additional income for those on low earnings and serves as a gateway to other benefits.

- Attendance Allowance or Disability Living Allowance: Offers support for retirees with long-term health conditions.

These benefits, while smaller than the proposed £549, are immediately available and often under-claimed.

Psychological Benefits of Financial Security

Beyond finances, a reliable and substantial weekly income has profound psychological effects. Financial stress is a major contributor to health issues among the elderly. A guaranteed £549 weekly pension would provide peace of mind, allowing retirees to focus on family, hobbies, volunteering, and personal fulfillment rather than constant budgeting anxiety.

Monitoring Developments

For those over 60, staying informed is key. The Autumn Statement and Spring Budget are critical events where pension changes may be announced. Campaign petitions exceeding 100,000 signatures are debated in Parliament, keeping pressure on lawmakers to address pension adequacy.

Understanding Your Pension Forecast

Before relying on potential increases, it is wise to request a State Pension forecast. This provides a personalized estimate based on your National Insurance record and helps identify gaps or opportunities to maximize income. Knowing your baseline allows effective planning and a realistic assessment of what a £549 weekly pension would mean for your lifestyle.

Final Thoughts

The proposal for a £549 weekly State Pension for all over-60s represents a bold vision for retirement in the UK. It highlights gaps in the current system, the pressures of modern living, and the need to value senior citizens appropriately. While economic and political hurdles make immediate implementation unlikely, the discussion itself is vital, shaping the future of social security for decades to come.

For now, the most practical step for pensioners is to claim all entitled benefits, monitor policy updates, and prepare for potential future increases in the State Pension. Financial awareness and proactive planning remain the keys to a secure, dignified retirement.